The VAT Myth Many Retailers Still Believe

Jun 23, 2026

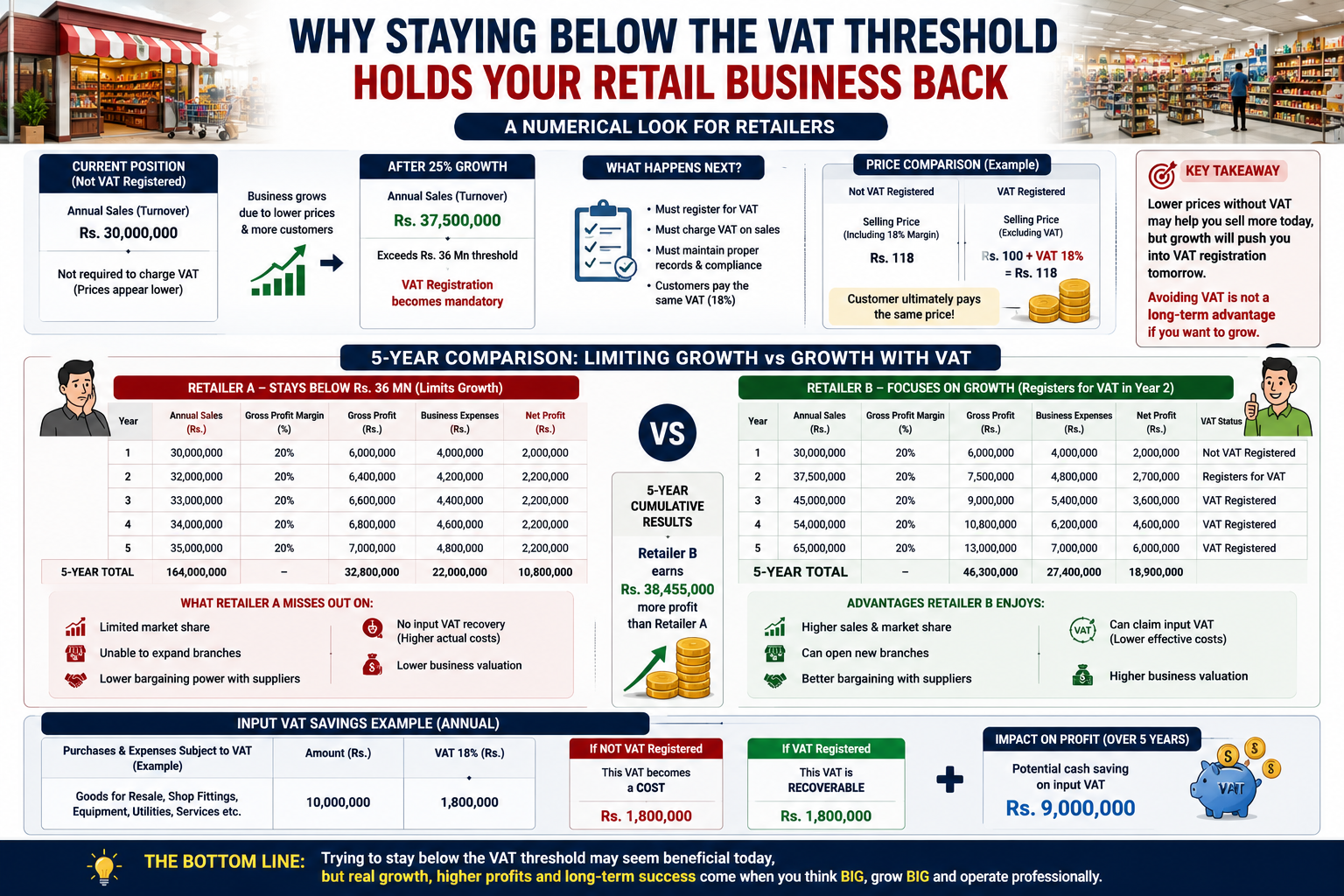

With the proposed reduction of the VAT registration threshold to Rs. 36 million per annum effective from 01 July 2026, many Sri Lankan retailers are reassessing their pricing strategies and growth plans.

One common argument frequently heard among small retailers is:

"Why should I register for VAT? Since I am not VAT registered, I do not have to charge VAT on my sales. Therefore, I can sell at a lower price than VAT-registered competitors."

At first glance, this argument appears reasonable. However, when viewed from a long-term business growth perspective, the advantage may be far smaller than many retailers think.

The Short-Term Advantage

Assume a retailer's annual turnover is below Rs. 36 million and therefore he is not required to register for VAT.

Since he is not VAT registered:

- He does not charge VAT on sales.

- Customers may perceive his prices as lower.

- He may attract more customers.

- His sales volume may increase.

This creates the impression that remaining outside the VAT system is beneficial.

But there is an important question many retailers fail to ask:

What happens when the business becomes successful?

Success Creates a New Problem

Suppose a retailer currently records annual sales of Rs. 30 million.

Because of competitive pricing and increasing customer demand, sales grow by 25%.

Annual turnover becomes:

Rs. 30 Million × 125% = Rs. 37.5 Million

The retailer has now exceeded the proposed VAT registration threshold of Rs. 36 million.

As a result, VAT registration may become mandatory.

The very strategy that helped the retailer grow has now pushed him into the VAT system.

The Reality of a Growth-Oriented Business

Every business owner generally has one objective:

To increase sales and grow the business.

If a retailer deliberately keeps turnover below Rs. 36 million simply to avoid VAT registration, he is effectively limiting the growth of his own business.

This creates several challenges:

- Reduced market expansion.

- Lower profitability potential.

- Limited ability to open additional branches.

- Reduced bargaining power with suppliers.

- Smaller business valuation.

The business may remain comfortable, but it may never achieve its full potential.

The Hidden Cost of Staying Small

Many retailers focus only on the VAT that would be charged on sales.

However, they often ignore another important factor:

The cost of restricting business growth.

Consider two retailers:

Retailer A

- Keeps turnover below Rs. 36 million.

- Avoids VAT registration.

- Maintains existing customer base.

- Growth remains limited.

Retailer B

- Focuses on increasing sales.

- Expands product offerings.

- Improves systems and controls.

- Exceeds Rs. 36 million.

- Registers for VAT when required.

- Continues to grow.

After five years, Retailer B may have several times the turnover, profits, and business value of Retailer A.

The real question therefore becomes:

Is avoiding VAT worth sacrificing long-term growth?

Another Important Point Retailers Often Miss

A retailer who remains outside the VAT system cannot generally recover input VAT incurred on eligible purchases and expenses.

VAT paid on:

- Shop fittings

- Equipment

- Utilities

- Professional services

- Certain business expenses

may become part of the business cost.

A VAT-registered retailer may be able to recover eligible input VAT, reducing the actual cost burden.

Therefore, the comparison is not as simple as:

"I don't charge VAT, therefore I am cheaper."

The true financial impact depends on the entire business model.

The Mindset Shift Retailers Need

The objective of a business should not be to remain below a tax threshold.

The objective should be:

- Growing sales.

- Increasing profitability.

- Improving systems.

- Building credibility.

- Creating long-term business value.

A growth-oriented retailer will eventually exceed Rs. 36 million in turnover if the business is successful.

When that happens, VAT registration becomes part of the normal business journey rather than something to be feared.

Conclusion

Many retailers believe remaining below the VAT threshold gives them a permanent competitive advantage because they do not have to charge VAT on their sales.

However, if the business has a genuine growth mindset, increasing sales will eventually push turnover beyond the Rs. 36 million threshold, resulting in VAT registration becoming unavoidable.

Rather than focusing on how to stay below the threshold, retailers should focus on how to build stronger, larger, and more profitable businesses. In the long run, sustainable growth often creates far more value than any temporary advantage gained from remaining outside the VAT system.