Comprehensive Guide to VAT on Digital Services in Sri Lanka

Jul 05, 2026

Understanding the New Digital Service VAT Framework under the Value Added Tax (Amendment) Act, No. 14 of 2026

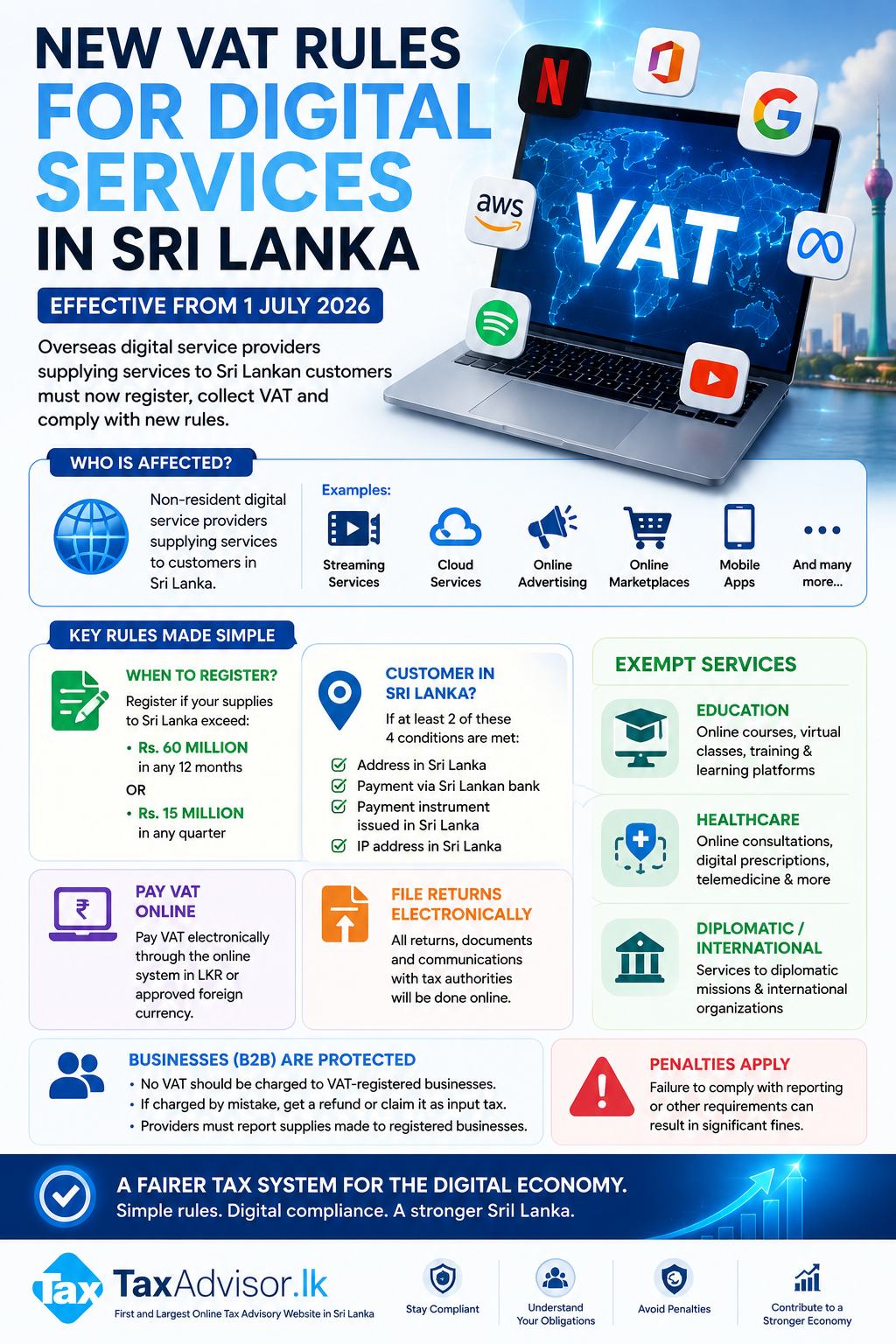

Sri Lanka has taken a significant step towards modernising its tax system with the certification of the Value Added Tax (Amendment) Act, No. 14 of 2026. One of the most important changes introduced by this amendment is the establishment of a comprehensive VAT framework for digital services supplied by non-resident persons through electronic platforms.

With effect from 1 July 2026, many overseas digital service providers supplying services to customers in Sri Lanka will be required to register for VAT, collect VAT, and comply with the provisions of the Value Added Tax Act.

This article explains the key provisions introduced by the amendment in a practical manner.

Why Was This Amendment Introduced?

The rapid growth of the digital economy has resulted in Sri Lankan consumers increasingly purchasing services from overseas digital platforms. While local businesses providing similar services have always been subject to VAT, many foreign service providers operated outside the Sri Lankan VAT system.

The amendment seeks to:

- Create a level playing field between local and foreign service providers.

- Expand the country's tax base.

- Align Sri Lanka with international taxation practices adopted by many other jurisdictions.

- Improve tax compliance within the digital economy.

Effective Date

The provisions relating to non-resident digital service providers become effective from:

1 July 2026

Accordingly, supplies made on or after this date are subject to the new rules.

What Are Digital Services?

The Act introduces the concept of digital services supplied through an electronic platform.

Although the Act does not provide an exhaustive list, digital services generally include services supplied over the internet without the physical presence of either party.

Examples include:

- Online software subscriptions

- Cloud computing services

- Streaming platforms

- Online advertising services

- Mobile applications

- Digital marketplaces

- Online gaming subscriptions

- Website hosting

- Artificial Intelligence platforms

- Subscription-based digital content

What Is an Electronic Platform?

An electronic platform refers to an online system through which services are supplied electronically.

Examples include:

- Websites

- Mobile applications

- Online marketplaces

- Cloud platforms

- Digital interfaces operating through the internet

Who Is Considered a Non-Resident Person?

A non-resident person means a person who supplies services but does not have a fixed place of business in Sri Lanka.

Accordingly, many international digital service providers fall within this definition.

When Must a Non-Resident Register for VAT?

Registration becomes compulsory once either of the following thresholds is met.

Annual Threshold

Where the total value of digital services supplied to persons in Sri Lanka exceeds:

Rs. 60 Million (or its foreign currency equivalent)

during any consecutive twelve-month period.

Quarterly Threshold

Registration is also required if the value of supplies:

Exceeds or is likely to exceed Rs. 15 Million

during any calendar quarter.

Time Limit for Registration

Once liable for registration, the non-resident supplier must submit an electronic application to the Commissioner-General within three months.

The registration process will be carried out electronically in the prescribed manner.

How Is a Customer Considered to Be Located in Sri Lanka?

The Act introduces objective tests to determine whether the recipient is located in Sri Lanka.

A recipient is treated as being in Sri Lanka if at least two of the following conditions are satisfied:

- The billing, residential or business address is in Sri Lanka.

- Payment is made through a Sri Lankan bank or financial institution.

- The payment instrument (such as a credit or debit card) was issued in Sri Lanka.

- The IP address of the device used for the transaction is located in Sri Lanka.

This two-factor approach helps reduce uncertainty and strengthens the integrity of the system.

Payment of VAT

The amendment introduces a fully electronic compliance framework.

VAT must be paid through:

- The Inland Revenue Department's online system; or

- Any electronic payment facility approved by the Commissioner-General.

Payments may be made:

- In Sri Lankan Rupees; or

- In approved foreign currencies remitted to a designated bank account.

Electronic Filing of Returns

Registered non-resident providers are required to:

- File VAT returns electronically.

- Submit documents electronically.

- Receive notices and communications electronically from the Inland Revenue Department.

This eliminates the need for physical documentation and simplifies compliance for overseas suppliers.

Special Rules for VAT-Registered Businesses (B2B Transactions)

The Act recognises that VAT should generally not become an additional cost for VAT-registered businesses.

Accordingly, special rules apply where digital services are supplied to a VAT-registered person.

VAT Should Not Be Charged

Where the recipient is already registered under the VAT Act, the non-resident supplier should not charge VAT.

This prevents unnecessary duplication of VAT.

If VAT Is Charged by Mistake

If VAT has been charged incorrectly:

- The supplier should refund the VAT to the registered customer.

If the VAT has already been remitted to the Inland Revenue Department:

- The registered Sri Lankan recipient may claim the amount as input tax, subject to the provisions of the VAT Act and supported by the supplier's invoice.

Reporting Requirement

Non-resident suppliers are also required to submit a simplified statement to the Commissioner-General containing details of supplies made to VAT-registered persons.

The statement includes:

- Taxpayer Identification Number (TIN)

- Name of the recipient

- Value of supplies made

This enables the Inland Revenue Department to verify input tax claims.

Exempt Digital Services

Not all digital services are taxable.

The amendment specifically exempts several important categories.

Educational Services

These include:

- Online courses

- Virtual classrooms

- Webinars

- Online training programmes

- Learning Management Systems (LMS)

Healthcare Services

Examples include:

- Telemedicine

- Online medical consultations

- Digital prescriptions

- AI-assisted medical diagnostics

Diplomatic and International Organisations

Digital services supplied to:

- Diplomatic missions

- International organisations

- Other institutions specified under written law or government agreements

remain exempt from VAT.

Cancellation of Registration

The Commissioner-General may cancel the VAT registration of a non-resident supplier where:

- Business operations have ceased for more than six months; or

- The supplier no longer meets the registration threshold.

Penalties for Non-Compliance

Failure to comply with the new requirements may result in significant penalties.

Examples include:

- A penalty of up to Rs. 50,000 for failing to comply with the reporting requirements relating to supplies made to VAT-registered persons.

- Higher penalties under the VAT Act for tax evasion, fraudulent refund claims, or other serious offences. Certain offences introduced under the amendment may attract penalties of up to Rs. 1,000,000 for applicable periods commencing on or after 1 October 2025.

Practical Impact of the Amendment

The new digital service VAT framework is expected to have a significant impact on both overseas suppliers and Sri Lankan consumers.

Non-resident digital service providers supplying services to Sri Lankan customers should carefully assess whether they meet the registration thresholds and ensure that their billing systems comply with the new VAT requirements.

Sri Lankan businesses registered for VAT should also review their procurement of overseas digital services to ensure that VAT is correctly applied and that available input tax credits are properly claimed.

The amendment represents another important milestone in Sri Lanka's ongoing digitalisation of tax administration and aligns the country's VAT system with internationally accepted practices for taxing the digital economy.

Conclusion

The Value Added Tax (Amendment) Act, No. 14 of 2026 introduces a comprehensive framework for taxing digital services supplied by non-resident persons through electronic platforms. From 1 July 2026, overseas digital service providers exceeding the prescribed thresholds must register for VAT, file returns electronically, and comply with the new reporting obligations.

Businesses, professionals, and digital service providers should familiarise themselves with these provisions at an early stage to ensure full compliance and avoid unnecessary penalties.

TaxAdvisor.lk will continue to publish practical guidance and updates on the implementation of these provisions as further directions and administrative guidelines are issued by the Inland Revenue Department.