Why Many Manufacturers Should Reconsider Avoiding VAT Registration from 01 July 2026

Jun 22, 2026

The reduction of the VAT registration threshold from Rs. 60 million per annum to Rs. 36 million per annum with effect from 01 July 2026 is expected to bring thousands of additional Sri Lankan businesses into the VAT system. While many discussions focus on traders and service providers, the impact on manufacturers deserves special attention.

For many years, a significant number of small and medium-sized manufacturers have intentionally remained below the VAT threshold due to concerns about compliance obligations. However, the question businesses should ask today is not whether VAT registration creates additional work, but whether remaining outside the VAT system is actually costing them money and limiting their growth.

Common Myths Among Sri Lankan Manufacturers

Myth 1: VAT Registration Creates Too Much Compliance Cost

Many manufacturers believe VAT registration means additional paperwork, VAT returns, tax invoices, reconciliations, and possible tax audits.

While compliance requirements certainly increase, every growing business eventually needs proper accounting records regardless of VAT registration. In fact, many manufacturing businesses already maintain records for inventory management, bank facilities, supplier management, and internal controls.

The real issue is not VAT compliance but whether the business is prepared to operate professionally.

Myth 2: Staying Outside VAT Keeps Things Simple

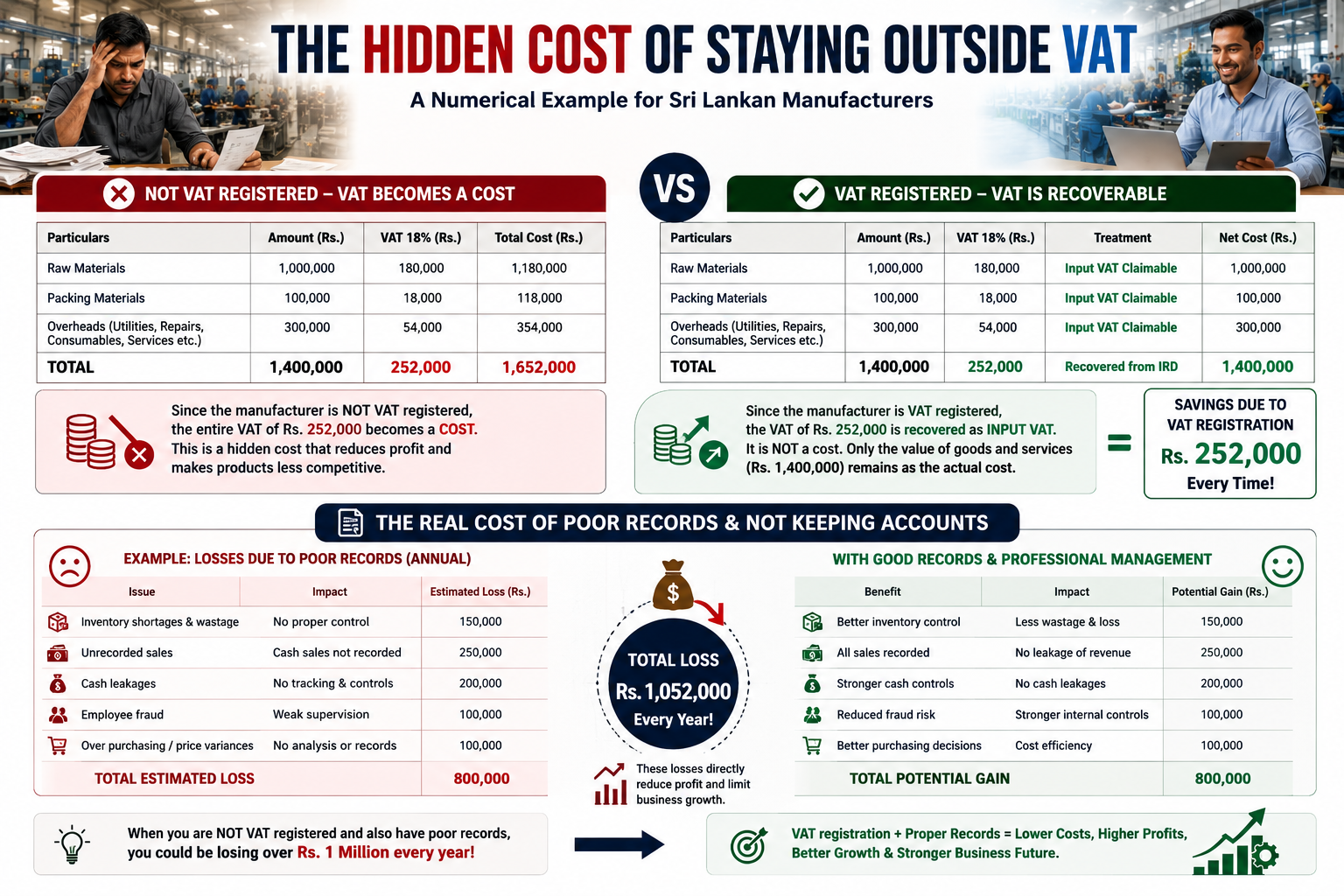

In practice, many business frauds and financial leakages occur because proper records are not maintained.

Manufacturers who operate without structured accounting systems often face:

- Inventory shortages

- Unrecorded sales

- Cash leakages

- Employee fraud

- Difficulty identifying profitable products

- Weak internal controls

VAT compliance indirectly forces businesses to improve documentation and record-keeping practices, resulting in better business management.

Myth 3: Remaining Small Helps Avoid Tax

Many manufacturers intentionally limit their reported turnover to remain below tax thresholds.

However, this creates a different problem.

When sales are not fully recorded:

- Financial statements become unreliable.

- Bank borrowing capacity reduces.

- Investor confidence decreases.

- Business valuations remain low.

- Expansion opportunities become limited.

A business that does not properly declare its turnover may save tax in the short term but often sacrifices long-term growth opportunities.

What Happens if a Manufacturer Remains Outside the VAT System?

The biggest disadvantage is the inability to recover input VAT.

Most manufacturers incur VAT on:

- Raw materials

- Packing materials

- Machinery repairs

- Factory consumables

- Professional services

- Utility-related costs

- Transportation services

When a manufacturer is not VAT registered, VAT paid on these purchases becomes part of the cost of production.

As a result:

- Production costs increase.

- Profit margins decrease.

- Cash flow becomes tighter.

- Products become less competitive.

This hidden cost is often ignored when businesses compare the advantages and disadvantages of VAT registration.

Key Advantages of VAT Registration for Manufacturers

1. Ability to Claim Input VAT

This is often the single biggest benefit.

A VAT-registered manufacturer can generally recover VAT incurred on eligible business purchases and expenses.

For manufacturers with significant raw material purchases, the savings can be substantial.

Instead of treating VAT as an additional cost, it becomes a recoverable tax.

2. Reduced Cash Flow Pressure

When input VAT can be recovered, businesses avoid carrying VAT as a permanent cost.

This improves:

- Working capital

- Cash flow management

- Inventory financing

- Profitability

For manufacturers operating on tight margins, this can make a significant difference.

3. Better Business Growth Opportunities

VAT registration often encourages businesses to:

- Maintain proper accounting records.

- Declare actual turnover.

- Improve financial reporting.

- Build credibility with banks and investors.

Many large customers and corporate buyers also prefer dealing with VAT-registered suppliers because it simplifies their own VAT recovery process.

As a result, VAT registration can open doors to larger contracts and new markets.

4. Improved Business Discipline

VAT compliance requires businesses to maintain:

- Tax invoices

- Purchase records

- Sales records

- Inventory documentation

Although this may initially appear burdensome, it often strengthens business controls and decision-making.

The result is usually a more organized and professionally managed business.

The New Reality from 01 July 2026

With the VAT registration threshold proposed to reduce to Rs. 36 million annually and Rs. 9 million per taxable period, many manufacturers that previously remained outside the VAT net may now become liable for registration.

Businesses should therefore evaluate:

- Whether they exceed the new threshold.

- The amount of input VAT currently absorbed as a cost.

- Whether major customers prefer VAT-registered suppliers.

- Whether improved financial reporting could support future growth.

Conclusion

Many Sri Lankan manufacturers traditionally view VAT registration as a compliance burden. However, in reality, the inability to recover input VAT may be costing them far more than the compliance costs they are trying to avoid.

The reduction of the VAT threshold from 01 July 2026 should not be viewed purely as an additional tax obligation. For many manufacturers, it may be an opportunity to improve record keeping, strengthen internal controls, enhance credibility, recover input VAT, and create a stronger platform for long-term business growth.

The businesses that treat VAT registration as a strategic business tool rather than merely a tax requirement are likely to be better positioned for sustainable growth in the years ahead.